TowerWatch #7: The Return

TowerWatch is back for 2020, and will be in your inbox every week for the foreseeable future. Hope everyone is having a great start to the new year — I know the markets are!

Three things you should know:

One: The Major Themes of 2020

2020 is already off to a good start. If Bitcoin holds current levels (+20% YTD), this will be Bitcoin’s best start to a year since 2013. Past Bitcoin, the broader markets are finally finding new attention with Bitcoin dominance flattening with slight downward trend despite the overall market trading up (the first time we’ve seen this combination since mid 2019 — indicating real capital inflow rather than reshuffling).

Outside of the markets, fundamentals are growing nicely as well. Bitcoin hash rates are now at an all time high, ETH 2.0 is chugging along nicely and is expecting the transition over to begin this year, and we’re closer than ever to interoperability between blockchains courtesy of Cosmos and its coming IBC protocol.

Over the course of the last two years, much of the froth of 2017 has died out, and we’re now left with higher quality projects and visions. Smart money has moved away from cheap token flipping, and capital in the space is quickly diverting towards better quality entrepreneurs and companies.

There’s a lot to be excited about in 2020, but three major themes stand out as dominant narratives over the next year:

Usable Products

Bitcoin as a Macro Asset

Institutionalization

Starting with #1. If 2019 was the year of building then 2020 will be the year of deliverance. Slowly the cryptocurrency world is producing useful products outside of decentralized money, and people are beginning to notice. In 2019, Synthetix proved to be a great example of how real world usage can lead to outsized returns. Their synthetic asset platform has quickly become the second largest decentralized finance platform due to their innovative token economics, great product, and easy user experience. In the process, they delivered a 20x return over the course of the year.

It seems that the real returns moving forward will be less driven by protocols with visions of grandeur and more by projects that deliver on product usage. Looking ahead to 2020, there are already some launches in the works:

Decentraland launching a virtual world on the Ethereum blockchain in February.

Augur releasing V2 of their prediction market soon (which should dramatically improve usability).

The Brave team getting to 10m uses, and introducing a new products such as the newly proposed decentralized VPN.

The second theme (Bitcoin as a macro asset) has become a hot topic over the last few weeks due to recent geopolitics. It’s becoming more evident to individuals outside of the cryptocurrency world that Bitcoin is beginning to act more mature every day. The recent price action in reaction to an increase in US - Iran tensions hammered home the point that Bitcoin can act as a hedge in times of turmoil. As 2020 stands an interesting year for geopolitics and monetary policy (with the rise of China and continued central bank easing), it makes sense that the discussion around Bitcoin as a macro asset will only continue to grow.

Lastly, the recent institutionalization of this asset class cannot be understated. As recently as 2017, there was no way for a traditional market participant to easily short Bitcoin. There was no way to place large bets on Bitcoin volatility, and there were no qualified custodial solutions for individuals that needed them. The idea of a digital, blockchain based currency was foreign to the majority of the world.

Now more than ever, there are a large number of ways to invest in the cryptocurrency space. There are plenty of registered broker dealers to source large buyers, a good amount of reputable custodial solutions, and now there are even structured products so one can tailor their exposure to the market. All of this development makes the cryptocurrency world infinitely more attractive to institutions. Now the pertinent question is whether money will flow into the system. In 2018 and 2019 we built the rails — now that the rails are here, we need to see the flow.

Two: The Macro Case for Bitcoin (Again!?)

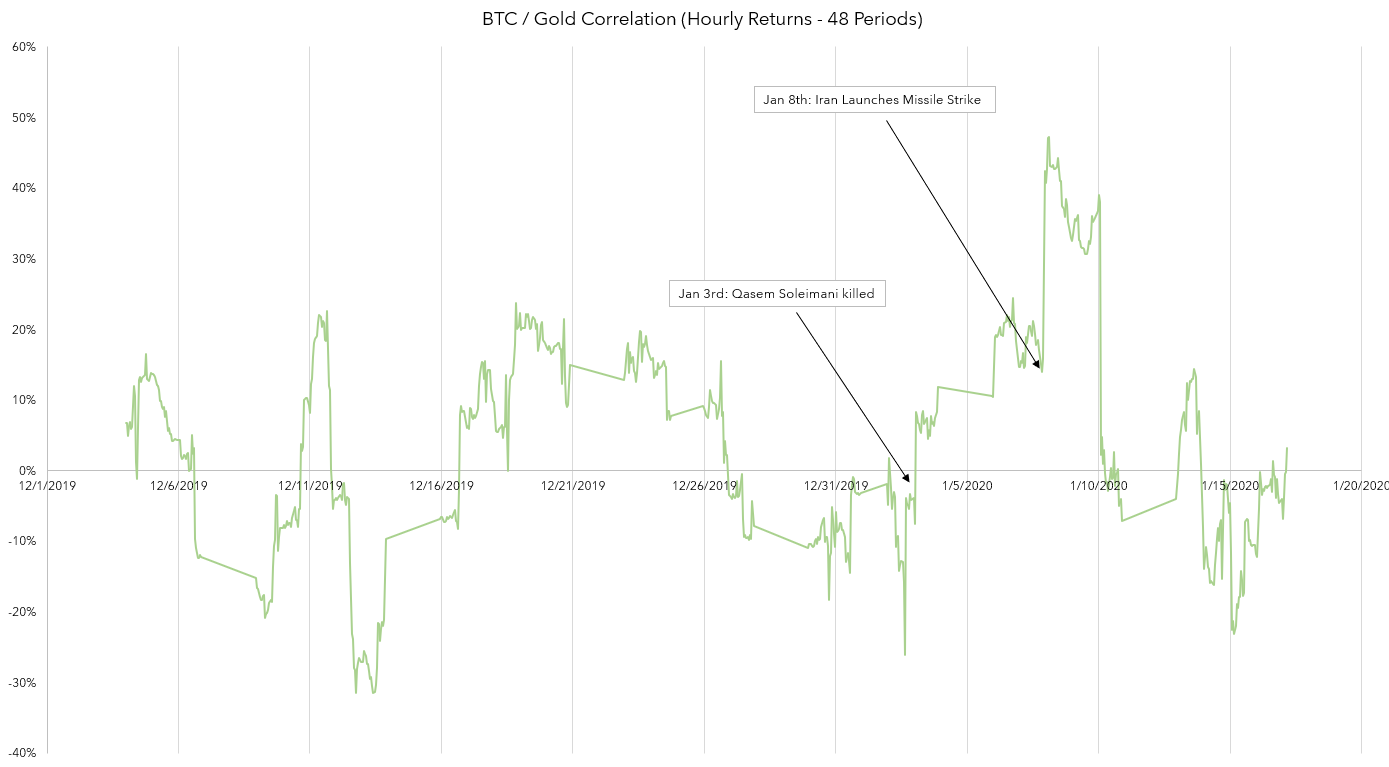

In previous editions, we’ve talked about the macro case for Bitcoin from a variety of different angles, all mostly theoretical. For the first time since starting TowerWatch, Bitcoin experienced a live test of this thesis and passed with flying colors.

Of course, we’re talking about Iran. On January 3rd, it was reported that Qasem Soleimani was killed by a U.S drone strike, and Bitcoin ticked up on the news. Five days later, Iran launched a missile strike at an American base in retaliation, and Bitcoin rallied alongside Gold. The next day, when Trump announced to the world that no Americans were hurt (and implied that de-escalation was coming), Gold and Bitcoin sold off in unison.

Historically, Bitcoin’s volatility has been a blessing. While it’s true that there may have been times of reaction to macro events, it was always a game of speculation. The Cyprus bailout, the Yuan trade, instability in Argentina - all of these did coincide with Bitcoin moving up, but that movement could have easily been because Bitcoin is a highly volatile asset. There are plenty of potentially bullish events that elicit a reaction from Bitcoin.

That is what makes this Iran situation a little different. This was the first time Bitcoin reacted to a macro event in a way that is hard to write off as coincidence. Bitcoin’s hourly correlation with Gold shot up significantly after Jan 3rd, and for the next week they moved very closely. Recently they’ve started to diverge again, but the damage was already done and mainstream outlets were reporting that Bitcoin reacted to the Iran news, reinforcing the belief and making it more likely to occur again in the future.

At the risk of repeating myself, I find it important to weave together a few story-lines:

Bet against reflation (Bitcoin vs. Gold as an inflation hedge)

Hedge against irresponsible monetary policy

Bitcoin’s optimal conditions are isolated pockets of risk, but equities still do well

Bitcoin as a maturing asset

2020 seems to be concocting the perfect storm for Bitcoin. Central Banks around the world are ramping up aggressive monetary policy after cooling off for a year. The possibility of inflation is emerging again as the trade war with China heats up, and as Asia turns into a mature economic zone. Isolated risk is popping up again (War with Iran, India’s slowing economy), but in general, investors are still relatively risk on (see: NASDAQ returns YTD). The above, combined with the increasing professionalism of the Bitcoin world and increasing ease of access is pointing to a very promising 2020.

Three: Payment Rails & Digital Dollars

Something interesting happened this week. The Former CFTC chairman Chris Giancarlo announced the formation of the Digital Dollar Foundation, a non-profit dedicated to developing a framework for practical steps that can be taken to establish a dollar central bank digital currency. Fmr. Chairman Giancarlo stated in the announcement of his initiative that “A digital dollar would help future-proof the greenback and allow individuals and global enterprises to make payments in dollars irrespective of space and time,” and that the aim of the project is to “catalyze a digital, tokenized U.S. currency that would coexist with other Federal Reserve liabilities and serve as a settlement medium to meet the demands of the new digital world and a cheaper, faster and more inclusive global financial system.” Digital fiat currencies, colloquially known in the crypto industry as Central Bank Digital Currencies or CBDC’s, are a growing trend among Central Banks, which we discussed in TowerWatch #4.

A refresher on the current landscape of CBDC’s:

So how does the Digital Dollar compare to existing solutions or Bitcoin? Bitcoin, although ideal for transacting independent of a specific financial system, privately, and across borders, is not useful as a payment technology. Centralized services will be faster for general payments for the foreseeable future. Once such existing solution, Plaid, is a payment rails startup that allows application developers to easily integrate their products with the US Financial institutions. It was acquired by VISA for $5.3 bln this week. All it takes is a few lines of code and you’re done. Couldn’t be any easier, right? Payment rails companies such as Plaid, Visa, MasterCard, Stripe, and Paypal have long offered products that allow for transactions between users on their systems entirely digitally. So where do Digital Dollars come in and how is it different?

The Digital Dollar is perfect for economic coordination at the macro level. It reduces transaction times and costs, increases the effectiveness of enforcing AML laws and allows (on the slightly more worrying side for freedom lovers) greater insight in every transaction made using that currency. Cash is currently an entirely private way to transact. An entirely digital dollar reduces the likelihood of tax and sanction evasion, money laundering, racketeering and other financial crimes. An entirely digital world is ideal for policy makers, law enforcers, and regulators.

Why this matters: Conflict between decentralized, corporate and state-run currencies and payments infrastructure will heat up in 2020. The dollar is a major source of power for the United States. Policy-wise, it makes sense for the U.S to introduce their own digital currency to retain that dominance, as well as encourage the adoption of decentralized versions, because the main competitor to US hegemony is a new global financial order that excludes the United States. This threat does not come from Bitcoin, as it is permissionless, but from China which can and will restrict access to its financial system for geopolitical goals. It seems likely that China would restrict its citizens from adopting a digital dollar. China’s strict capital controls and introduction of the Digital Yuan will pose a direct threat to US interests. As there is no way to prevent this, Fmr Chairman Giancarlo, among others, have realized the US needs to compete by introducing their own version.

Things That Happened:

General

Gemini ventures into insurance business - launches 'Nakamoto' to provide $200M crypto coverage

Airlines must pay for fuel in Petro, says Venezuela's Maduro

Regulatory

Oklahoma Lawmaker Proposes State-chartered Crypto Depository

US Government Files Lawsuit Against Operators of Blockchain Terminals $30m ICO

Markets

Market Outlook:

The market is back with a vengeance over the last month, with BTC almost ~40% off its local low. Over the weekend, we saw Bitcoin push up to a high around ~9.2, before dramatically falling early Sunday morning to ~8.6k, where we are currently trading. We had ~108m long liquidations on the move, as late longs were punished severely. The bullish market structure is still intact, but it’s now clear that the 200DMA is acting as significant resistance.

We’re currently at a critical level. Holding 8600 would lend confidence to the idea that this drop was just longs getting structurally flushed from the market, as opposed to a break in the trend. If we lose 8600, 7700-7800 are the next strong support levels, with 8200 acting as a potential weak support.

Key Levels:

Support: 8600 / 8200

Resistance: 8900 / 9200

Some interesting data points:

CME leveraged funds flipped from long to short right before the recent drop

Skew has come back in line to favor calls after two weeks of frontend skew favoring puts

We are seeing a large buildup of open interest, and funding rates are steadily increasing, signifying a return of short term traders

We’ve seen volatility return to the altcoin market, with many coins coming in at over 100% realized vol to start the year.

Overall Market: The last week has seen above average performance from a basket of “halving” coins. In the first six months of 2020, the cryptocurrency markets are experiencing a few different halvings. We have BitcoinSV in March, Bitcoin Cash in April and Bitcoin itself in May. Later in the year, Zcash will have it’s own halving which will dramatically reduce the inflation rate (which currently stands ~30%!).

Staking coins, the investor darling over the last two months, have lost their shine as faith in market turned positive. It makes intuitive sense — when the market is experiencing turmoil, yield becomes very attractive. As investors see the market turning green, they flee from their safe yield to high risk assets. Why would you turn down potential 40% returns in a day, like ZEC and BCH posted over the last week?

Moving forward, it seems as though alts want to act as a high beta version of Bitcoin. We’re near two year lows in alt/btc ratios, and many overlooked pairs have recently found love. It wouldn’t be surprising to see this persist throughout 2020.

What We’re Thinking:

If you’ve forayed into the wonderful world of Bitcoin futures, you’ve probably noticed a few things. The first thing you probably noticed was the tremendous amount of leverage allowed by exchanges. 100x leverage on an asset that often realizes over 100% annualized volatility is pretty wild! If you dug a bit deeper, you may have found the March and June futures.

If you were looking closely at the prices, you may have seen that the March future was trading almost ~300 dollars above spot on Saturday, which translates to a 14% annualized return if you shorted the march future against buying spot bitcoin. What gives, is this free money?

Well, just three weeks ago the annualized implied interest rate on the BitMEX March 27th BTC future was ~7%. On Saturday, that had widened to ~14%. Now it’s back to ~8%.

What caused this rapid increase? Why is there a spread in the first place? Is this normal? Is it weird?

Well as it turns out, the spread you see on Bitcoin futures is actually a bit of an oddity — but the fact the spread itself exists is not!

The forward curve exists in the traditional markets, and is a function of three things (in the commodities markets):

Spot Price

Interest rates

Delivery & storage costs

Most BTC futures are cash settled, so we can ignore the delivery and storage costs for now. So here’s the formula for determining a cash settled futures price:

Futures Price = Spot Price × (1 + Risk-Free Interest Rate – Income Yield)

Now, Bitcoin doesn’t have an income, so we can simplify by just looking at the interest rate. Theoretically, the futures price should be equal to the spot price * the interest rate you can get for lending out Bitcoin. As of writing, estimated interest rates for BTC are ~2.5-3%, implying that the annualized return for the cash and carry trade (short future, long spot, collect different as price converges) should be the same. It’s not, and the reason usually given is simple -- counterparty risk. The market prices in the risk of holding your Bitcoin on an exchange, and therefore you are compensated for that additional risk.

That answer is not complete though. If counterparty risk is constant, and interest rates only account for a small part of the curve (and fluctuate only a small amount), there shouldn’t be large swings in the futures curve, but there are.

There are a few reasons for this:

Demand: When Bitcoin turns bullish, demand for long leverage grows significantly. Funding rates on the perpetual swap can sometimes become prohibitively expensive, and so demand for the futures goes as well (cheaper leverage than paying for funding on the perp). This is actually an inefficiency that should be arbitraged away, but the unpredictability of the funding rate makes it difficult to do so. When Bitcoin is bearish, demand for short leverage grows significantly and the opposite effect takes hold.

Opportunity Cost: In order to take advantage of the futures curve, you need to hold cash. If the March future curve is trading at ~14% annualized, you can capture that by shorting the future and buying spot bitcoin for a “free” 14% gain annualized. The issue here is if Bitcoin is in a bull market, one is sacrificing a tremendous amount in opportunity cost to take on this trade, which makes it marginally less interesting.

Operational Cost: Theoretically, there is plenty of cash on the balance sheets of firms outside crypto that could take advantage of this curve. Operationally, they are unlikely to view 14% as adequate compensation for the risk of the market, so they do not take advantage of the opportunity. The only individuals who take advantage are likely those that are crypto native (comfortable with the risk), and those types of market participants are unlikely to deploy capital to take advantage of the curve when Bitcoin is bullish (they would rather just own Bitcoin).

It’s unclear which is the driving force. In fact, there could be *more* arbitrageurs in the market when the spread blows out, not less as suggested above. It could be that the spread blows out entirely because of demand for the future. Anecdotally, many who play the curve exit the trade when Bitcoin turns bullish.