TowerWatch #10: The Great Sell-off

Welcome to the 10th edition of TowerWatch, a newsletter from BlockTower aimed at cutting through the noise of crypto markets. We have one purpose: be useful.

Three things you should know:

One: Moving Forward from Black Thursday

On Thursday, March 12th, Bitcoin experienced its 2nd biggest daily drop in history falling over 50% and trading briefly near 2019 lows of 3600 before rebounding sharply to the 5500 level.

Thursday’s move sharp introduced severe dislocations in the markets, with the BitMEX - Coinbase spread briefly blowing out to almost eight hundred dollars. The initial market move was driven by equities selling off in reaction to the President’s first real remarks to the nation about COVID-19 and saw Bitcoin fall from 7.7 -> 5.8 sharply triggering what would turn out to be the first round of BitMEX liquidations.

The way the BitMEX liquidation engine works is that it groups liquidations and exits them slowly, over time. As the liquidation engine continued to aggressively exit positions at market, buyers started evaporating at a fast pace, leaving little bid side liquidity, but a large amount of forced sell-side liquidity. This dynamic is what drove the majority of the second fall from 5.8k -> 3.6k.

At 5.8, leveraged longs jumped back in the market in some size, but quickly got overwhelmed by the sheer amount of liquidations that needed to be exited. Bitcoin fell swiftly through to the 4000’s, at which point many new buyers stepped in — but the liquidations had more to go. Many buyers in the high 4k’s got liquidated as well, as BTC fell an additional 25% to 3.6k adding additional pressure to the orderbook.

At the critical point in the night — with only 18m left on the ENTIRE bid side of the BitMEX orderbook, BitMEX shut down. The liquidations stopped, and Bitcoin was free to reverse sharply to the mid 5’s.

All told, over $1.5B in leveraged positions were liquidated on March 12th and 13th, flushing most of the leverage out of the market.

Many spot exchanges also experienced their highest daily volumes since 2017, indicating that this while this was a derivatives-led move, spot holders participated in the mayhem as well.

The repercussions of March 12th are still being felt in the markets. A large amount of liquidity has left the market, and as you can see from the chart below, spreads blew out significantly and a week later they remain elevated. A number of funds and market makers went out of business that night due to both critical infrastructure failures and risk management failures. Similar to the approach of traditional funds for the first few years post-2008 financial crisis, we expect hedging and risk management (and the ability to do it well) to be at the forefront of importance for managers at this moment.

Looking ahead: Currently, Bitcoin is trading at ~6400 and showing remarkable resilience in the face of equities selling off. Effectively, March 12th transferred Bitcoin from those with a short term, trading outlook to those who hold longer-term positions and have the balance sheets to withstand a sharp drop. In the long run, this deleveraging should have a stabilizing effect on BTC price. In the short run, we make no such claim.

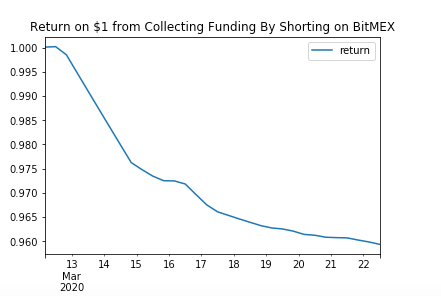

Interesting note: The aggressive liquidations on BitMEX and subsequent shorting over the next week kept the funding rate on BitMEX abnormally negative for an extended period of time, meaning that it has been quite expensive to short Bitcoin recently. If you held a short on BitMEX over the last week, you would have paid almost 4.5% in funding costs. If you shorted from the high (7.9k) and haven’t closed yet, you’ve given up 1/5th of your profit just to hold your position. Let this be a reminder: if you’re looking to short structural weakness, and plan to hold your position for an extended period of time — do it with futures (not financial advice).

Two: All Part of a Broader Market Sell-off

The last month in the markets has not been easy. Bitcoin price action has been profoundly influenced by the traditional markets and the threat of the novel coronavirus. Volatility has increased dramatically for both the S&P 500 and Bitcoin, with the S&P actually realizing volatility levels higher to the prior 6 months of Bitcoin vol.

Here’s a recap of the carnage:

Equities trading about ~35% off their 2020 highs

VIX posting an all-time high of 83

Oil falling 50% to multi-decade lows

Despite Bitcoin exhibiting low correlation to almost all assets over its 10-year life span, the market shock of the last month has seen Bitcoin trade closely with the overall market — namely, it’s gone down. Bitcoin’s 30-day correlation to the S&P is now 0.6, far above the previous all-time high of 0.32. At first, this may sound alarming if you have heard that Bitcoin may act as a global hedge. In reality, everything sells off in a deflationary crisis, because cash quickly becomes king.

A strong analogy is to gold during and around the 2008 financial crisis. Gold was in a secular bull trend heading into the 2008 crisis. Many expected it to continue to act as an “armageddon hedge” or as a hedge on central bank money printing, yet from August to November 2008, Gold sold off almost 30%. It then resumed its bull trend with an even steeper slope. In the early days of a crisis, the only thing investors reach for is cash. Often assets that theoretically might perform well are sold down to meet margin requirements and cash needs. We expect Bitcoin to act similarly in this crisis as gold performed in the last. It’s selling off with equities now but will likely benefit disproportionately when markets stabilize.

The market impact of the coronavirus caused the US government to take a series of actions that hasten fiat depreciation.

Over just the last 10 days, the Federal Reserve has

Cut interest rates to zero

Announced intention to restart QE, first with $700B — now with no cap at all!

Eased access to FX swap lines to allow foreign banks to borrow dollars at a cheaper rate

Opened up $1T in available commercial paper

Put $1.5T to work in the repo markets

Why this matters: All of the actions above feed into general worries of inflationary regimes and monetary devaluation, which are major narratives for Bitcoin appreciation. As a hard-capped currency Bitcoin is well-positioned for those that are now expecting inflation.

The best-case scenario for Bitcoin is for central banks globally to continue pushing liquidity into the system and for continued fiscal stimulus, with the health crisis mitigating relatively quickly. This would leave a deluge of money in the system once the primary deflationary effects of the crisis pass. Of course, the elephant in the room is COVID-19. If the virus holds the US economy captive for an extended period of time, it’s possible that the demand shock would be enough to offset the influx of new money into the system.

Three: The Fragility of Early Systems

Last week, MakerDAO, a decentralized lending and stable coin protocol built on Ethereum, experienced turmoil. During one of the sharpest market drawdowns in crypto’s history with BTC and ETH down over 50%, MakerDAO failed to perform a key collateral auction function that capitalizes the system due to congestion on the Ethereum network. The result of the failure was that the MakerDAO system incurred significant loss, and faced a multi-million dollar collateral shortfall.

The auctioning of liquidated collateral used to back the DAI-denominated debt issued by the system is essential to its continued operation. MakerDAO is governed by MKR token holders who vote on risk parameters within the system. As a result of last week’s shortfall, new MKR was auctioned to investors on Thursday and Friday. This auction exchanged DAI for freshly minted MKR which inflated the supply and punishes MKR holders for the failure to mitigate risk properly. Many in the community have pointed to Black Thursday’s events as a reason to doubt MakerDAO and the DeFi ecosystem, as they believe it shows the flaws of the approach and early decentralized systems. However, early turmoil is not unique to decentralized systems with many other early systems experiencing crises only to survive, iterate and then grow larger than before.

Complex systems have a long history of stress tests that lead to near failure. Anything sufficiently complex and new is subject to this risk. From early legal systems and governments to code, applications, and financial markets, complex networks undergo iterations to survive and thrive.

A famous example of this is the early internet and the applications built on it as the new millennium approached in 1999. Dubbed Y2k, it refers to events relating to the formatting and storage of calendar data for dates beginning in the year 2000. Problems were anticipated and arose because many programs represented four-digit years with only the final two digits – making the year 2000 indistinguishable from 1900. It was one of the biggest collapses that never happened. Over $300 billion was invested to upgrade computer networks to ensure that Y2K didn’t turn into the catastrophe that was expected. Early designers of applications failed to take into account an obvious risk which almost resulted in the failure of essential services to society.

Space flight and the spaceship are complex systems with numerous early challenges. The unique combination of knowledge to build the system included physics, material science, computer, and hardware engineering, and took decades to perfect. Even after the successful functioning of the spaceship and space flight “systems” for many decades, one fateful day in 1986 led to the Challenger exploding, killing the 7 crew onboard. This grounded the US Space Shuttle fleet for 3 years during which various safety measures, a solid rocket booster redesign, and a new policy on management decision making for future launches were implemented. The iteration and innovated as a result of this event provided an opportunity to improve systems and prevent future tragedies.

New governments are complex systems made up of laws, customs, and cultures that create numerous challenges. The founding of the United States is one such example. As an early nation attempting to separate from the British empire, the 13 colonies ratified, during the second Continental Congress in 1777, the Articles of Confederation, a loose system of government that prioritized state sovereignty over a strong federal government. Due to infighting between states and the continued threat from the British, the Articles of Confederation failed. The states then advocated for the abolishment of the Articles which eventually lead to a stronger more unified nation under the Constitution ratified in 1788. The failure of the first approach led to the iteration that resulted in the Constitution that is still used more than 200 years later.

If complex decentralized systems are expected to succeed they must fail early and quickly, then adapt, before they can grow. Although MakerDAO failed to perform perfectly under stress this time, it has survived and adapted. One such adaptation was the introduction of USDC, a stablecoin issued by Circle and Coinbase, to act as collateral in the system. This is expected to help stabilize the price and reduce the likelihood of unexpected liquidations in the future. Challenging times required change and MakerDAO and its MKR governors responded. As with every system, we expect MakerDAO to continue to adapt in order for it to succeed and thrive.

Things Happen:

General

Regulatory

Markets

Market Outlook:

Today Bitcoin got a bounce from the Fed announcement of “unlimited” asset purchases, trading up almost 10% off its lows of the day. What’s interesting to note here is that the S&P trading down on the news (seemingly desperate for fiscal stimulus, not monetary), Bitcoin traded up and is holding the majority of its daily appreciation.

Gold also traded up significantly on the announcement, as the market seems to be anticipating inflation. Looking ahead, it’s likely that you will see the argument for Bitcoin shift in narrative from the “uncorrelated asset class” to “inflation hedge” argument.

Normally in this section, we’ll perform some rudimentary technical analysis to assess Bitcoin, but TA is relatively useless here for longer-term (read: 1-2 week) prognostications. Due to the emotional state of the market, levels are being respected on shorter timeframes, but have the potential to be torpedoed by macro announcements of stimulus, good/bad news on the virus front, or large policy decisions. While you navigate the markets, you should keep in mind that the best trade set up is likely to be tanked by things outside the chart in these times far more than usual.